It’s been said before and will continue to be said, that for most there are far more pressing concerns, be it their own health, the well-being of loved ones and friends, their own finances and if in the health and care sector, how to keep well whilst trying to help all those less fortunate than themselves. Whilst I think it’s important we remain mindful of the impact on the club and sport we love, I firstly want to wish everyone well, keep safe and look after each other as much as is possible.

Aside from the potential threat of relegation, football in the Premier League has been a one way street of ever increasing revenues, inflated values and for those involved in the game increasing rewards wholly out of kilter with reality and certainly value.

Revenues arose from secure sources – broadcasting, match day revenues, commercial and sponsorship. Fueled by those increasing revenues the value of players rose, inflating balance sheets, creating player trading profits (often covering operational losses) and proving rich picking grounds for those advisors and agents on the periphery of the sport.

All of this is strikingly similar to the finance sector in the mid-2000’s. Many football clubs (like banks then) have grown big on the wave of money entering the industry. Few (like the banks) are prepared for a massive business disruption.

Let’s examine the potential impact of Covid-19:

Season 2019/20

We are three quarters of the way through a season. There is little or no prospect of the season resuming. There should be little or no prospect. Nothing should deflect public resources until the virus is, as far as possible, eradicated. Until every vulnerable person is back to a position of safety and security, football has no right to even suggest a return.

Cashflow:

With no games being played cashflow is impacted immediately, although given the number of season tickets already sold, the impact is less than we might think.

So, looking at the average revenue per game and removing the season ticket revenues already received, the initial loss of cash flow for selected clubs per game is estimated at:

So potentially lost revenues ranging from £600,000 for Everton to £7.2 million for Liverpool between now and the scheduled end of the Premier League season. Anticipated progress in cup games for those still in competitions add to that figure.

When the Premier League recognises that no games can be played in front of paying spectators, given usual terms and conditions, all clubs will have to issue pro-rata refunds to season ticket holders

For Everton I estimate that would cost approximately £3 million in refunds, giving a total loss of ticket revenue of £3.6 million. By way of comparison, £17 million refund to season ticket holders (total loss of ticket revenues £ 22 million) for Manchester United and near £ 7.0 million for Liverpool (total loss of ticket revenue £14 million).

Costs:

Operating costs will fall during the period of inactivity which will obviously have a small positive impact on cash flow. For Everton, as a result of not travelling and no staging of matches, operating cost savings of 25% would amount to £2.5 million per quarter.

Additionally, cash flow will be assisted by a reduction in player wages. All match related bonuses are obviously currently on hold.

Commercial Arrangements and sponsorship:

It’s difficult to be accurate forecasting losses from commercial arrangements as each club (obviously) has different agreements with different commercial partners be they kit manufacturers, merchandising manufacturers and distributors to match day event organisers, caterers and food and beverage operators.

Almost all of these arrangements will operate under long-term contracts. Most will have a form of force majeure written in but typically such clauses are general by nature. Business interruption insurance may help, but often specific cover for pandemics will be required.

With regards to sponsorship the position is likely to be a little clearer with the potential for penalty clauses for non-fulfilled matches more obvious. Looking at the likely factors determining loss arising from commercial and sponsorship partners would include, the number of games not played, how many behind closed doors (if played, but unlikely), reduction in sponsor related activities and events including match days, number of appearances on domestic and overseas television and whether European competition is continued. Additionally, for the larger clubs, the cancellation of the usual lucrative end of season and pre-season tours to Asia and elsewhere will impact revenues hard – estimated up to £6 million.

Everton, almost counter-intuitively would be less affected than our major competitors given the high proportion of sponsorship income (£12 million pa) provided by USM. Having said that the timing of looking for a new shirt sponsor could hardly be more challenging.

One of the areas of concern to many clubs must be their reliance on betting company income. Many sectors are being hit hard, but the sports betting industry must be among the most impacted. Shirt sponsorship by betting companies is worth an estimated £68 million p.a. to Premier League clubs. The triple whammy of reduced name awareness, lack of sporting events and significant revenue issues for the gambling companies must have their lawyers reaching for the break clause in many cases.

Broadcasting revenues:

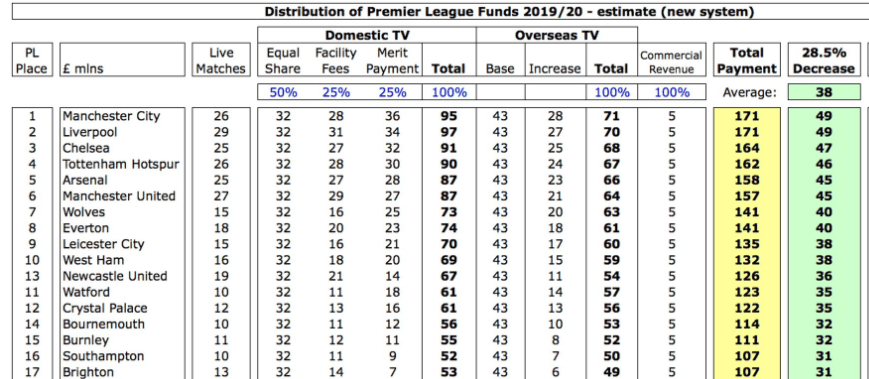

How this season is concluded (completed behind closed doors or voided) has clear financial impacts for all Premier League Clubs. The Athletic has reported potential penalties/withdrawal of income amounting to £762 million. Split equally that would amount to £38 million per club.

Swiss Ramble has put forward calculations based on pro-rata share of previous awards showing those that earn more would be penalised more (by virtue of a 28.5% reduction):

©Swiss Ramble

The impact of no Premier League product on broadcasters is worthy of much greater scrutiny than this article, but the longer the absence (quite correctly absent) the more difficult it is for broadcasters to continue drawing subscriptions and with advertising revenue obviously negligible cost recovery from the Premier League becomes a real option.

I wonder if the attitude of UK based broadcaster might differ from overseas broadcasters who have paid a huge price for a product which has not been delivered?

Equally, if as is expected and feared we enter a significant global recession, discretionary spending is usually hardest hit. Overseas, what can be more discretionary than subscribing to Premier League football? It’s difficult to imagine a scenario where many broadcasters will see the same levels of subscription, and indeed, broadcasting revenues in the next few years. Advertising and promotion (A&P) is usually hard hit by companies facing their own cash flow issues in times of recession.

Thus the financial impact of Covid-19 will have both short and longer term implications for football clubs. Clearly smaller clubs are going to be impacted and many very heavily, but not exclusively.

Premier League clubs, despite their rich revenue streams of recent years, are not likely to be well placed too. The pre-Covid set of accounts for many Premier League clubs are showing a trend of increasing losses. Lost revenues, quite possibly significant at up to 25% or more will only accelerate that trend.

For Everton lost revenue of that magnitude (perhaps as high £45 million net) would (as with all other clubs) seriously impact our P&L.

Without a relaxation of financial regulations either permitting greater losses or allowing new shareholder contributions, many outside of the top 6 will struggle.

Transfer values

Revenue reductions such as those suggested above will see a deflationary effect on asset values across football, especially if future broadcasting revenues remain under pressure. For clubs with a large inventory of players this is potentially damaging for a number of reasons.

In a deflationary environment future player contracts may reduce in value making players more reluctant to move if on highly rewarding existing.

Lower transfer values reduce player trading profits, a key component of many clubs’ P&L strategies in recent years.

Finally, a significant reduction in player values might see clubs introducing impairment charges to more accurately reflect the value of players.

Capital Projects

A background of falling revenues, increased losses, potentially the re-valuing of intangibles such as players and more specifically harder economic conditions in the future, in which to fill stadia with spectators and sell advertising is not ideal for major capital projects.

Bramley-Moore is to be funded by a combination of equity investment, sponsor/naming rights contributions and in the large part by debt. Whilst there is nothing to suggest that Moshiri’s commitment nor that of potential naming rights partners USM has in any way waivered, it has to be recognised that we are in a completely different economic scenario than at the time the planning application was made in late December 2019.

The club has spoken of their desire to use the private placement markets, particularly in the US, to fund their debt requirements. For many years investors seeking a higher yield than Government bonds, but still relatively high security have funded many companies in this manner. The most recent example in English football was Tottenham Hotspur’s conversion of bank debt into long term paper to the value of £525 million through the private placement market – all priced below 2.99%.

The recent crashing market and fear of global recession or worse, has impacted this debt market (as with all other corporate debt markets). The chart below reflects the change in yield. This is a reflection of growing concerns over companies’ inability to service their debt and in future, a requirement for a higher yield for new borrowers to reflect the increased risk to the investors. To be fair this takes us back to yields seen previously (end of 2018), however they’re much higher than end 2019.

The change in market conditions will almost certainly be reflected in the (as yet to be announced) debt arrangements secured by Everton. It may be that by the time planning permission is granted, market conditions have improved – equally the reverse is true.

Despite all the uncertainties above, football can’t be rushed back – not until the playing of professional football takes no resources needed elsewhere in the treatment of Covid-19, not until there’s no risk to any individual who would be involved in the playing or staging of the professional game.

Football is not as important as all that’s unfolding around us. Our concerns must be with our loved ones, friends and others in the hope that we all contribute to making Covid-19 as least damaging as possible whilst keeping our own safe. But inevitably we have to look at other matters too, and football, specifically Everton is one of those areas.

Good luck and stay safe!

Categories: Everton Finances